Self-Insuring for Long-Term Care

Self-insuring for long-term care certainly has it’s risks. But exactly how does it compare to affordable long-term care insurance? And which is better?

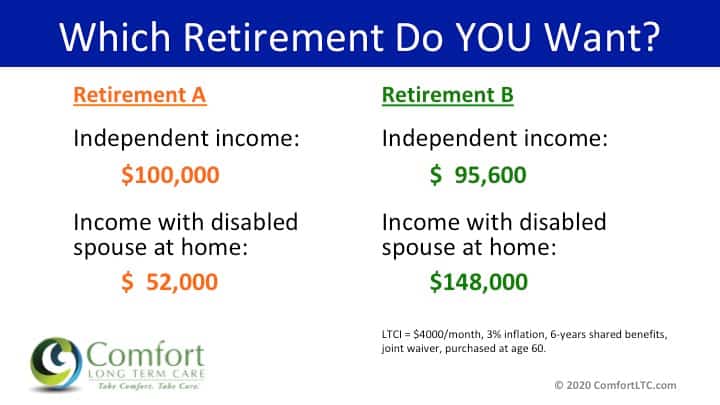

Retirement A:

Provides a great income and lifestyle while everything is going well…

But if one spouse needs care, part-time home care, could easily cost $4,000 per month.*

And what happens to the couple’s lifestyle, the still-independent spouse’s lifestyle? It’s cut in HALF!

You can’t make up the difference by taking more money from assets because this jeopardizes the viability of the entire financial plan. Self-insuring for long-term care may not be the best option.

Retirement B:

Assumes this 60-year-old couple purchased basic, affordable long-term care insurance that costs $4,400 per year ($367/month) to cover both.**

If one spouse is disabled, both policies’ entire premiums are waived AND it provides an EXTRA $4,000/month in tax-free benefits to pay for care.

The premium costs a few hundred dollars a month, but the benefits if one spouse needs care nearly TRIPLE the available income versus a self-funded plan! This certainly seems like the best option.

Genworth 2019 Cost of Care Survey

This article was originally published by Bill Comfort, CSA®, CLTC®, LTCCP on his website and re-posted with permission. ComfortLTC.com.

This article was originally published by Bill Comfort, CSA®, CLTC®, LTCCP on his website and re-posted with permission. ComfortLTC.com.

Which type of policy is right for you?

No phone required.

Custom quote in 2 hours.

Instant ranking of the 4 types of long-term care coverage.

Facebook Comments