Yugo Failed! Long Term Care Insurance Must Be Dead Now

Between 1985 and 1992, over 140,000 Yugos were imported into the United States. The Yugo rarely met emission standards, had an unreliable electrical system, and continually broke down. The joke went:

“Why does the Yugo come with a rear defroster?…..”

“so your hands stay warm when you push it.”

Needless to say, when Yugo pulled out of the U.S. market, no one was surprised and no one cared. Yugos accounted for less than 1% of auto sales.

Did the headlines read, “Collapse of Yugo Reveals Deep Problems Plaguing the Entire Auto Industry?”

Of course not. No newspaper would have written such a ridiculous headline. Yugo’s failures were caused by Yugo’s mismanagement.

Yet the Wall Street Journal described the pending liquidation of Penn Treaty (a small LTC insurance company with about 1% of the market share) as “highlighting the widespread problems that have plagued the industry…for more than a decade.” Nothing could be further from the truth!

The writer, Leslie Scism, does a good job of explaining how long term care insurers mispriced their policies in the 1990’s and early 2000’s. However, her article fails to point out the real reason for Penn Treaty’s demise. Penn Treaty’s mistakes went well beyond mispricing. Penn Treaty’s failure is because they ignored the federal guidelines for long term care insurance benefit triggers.

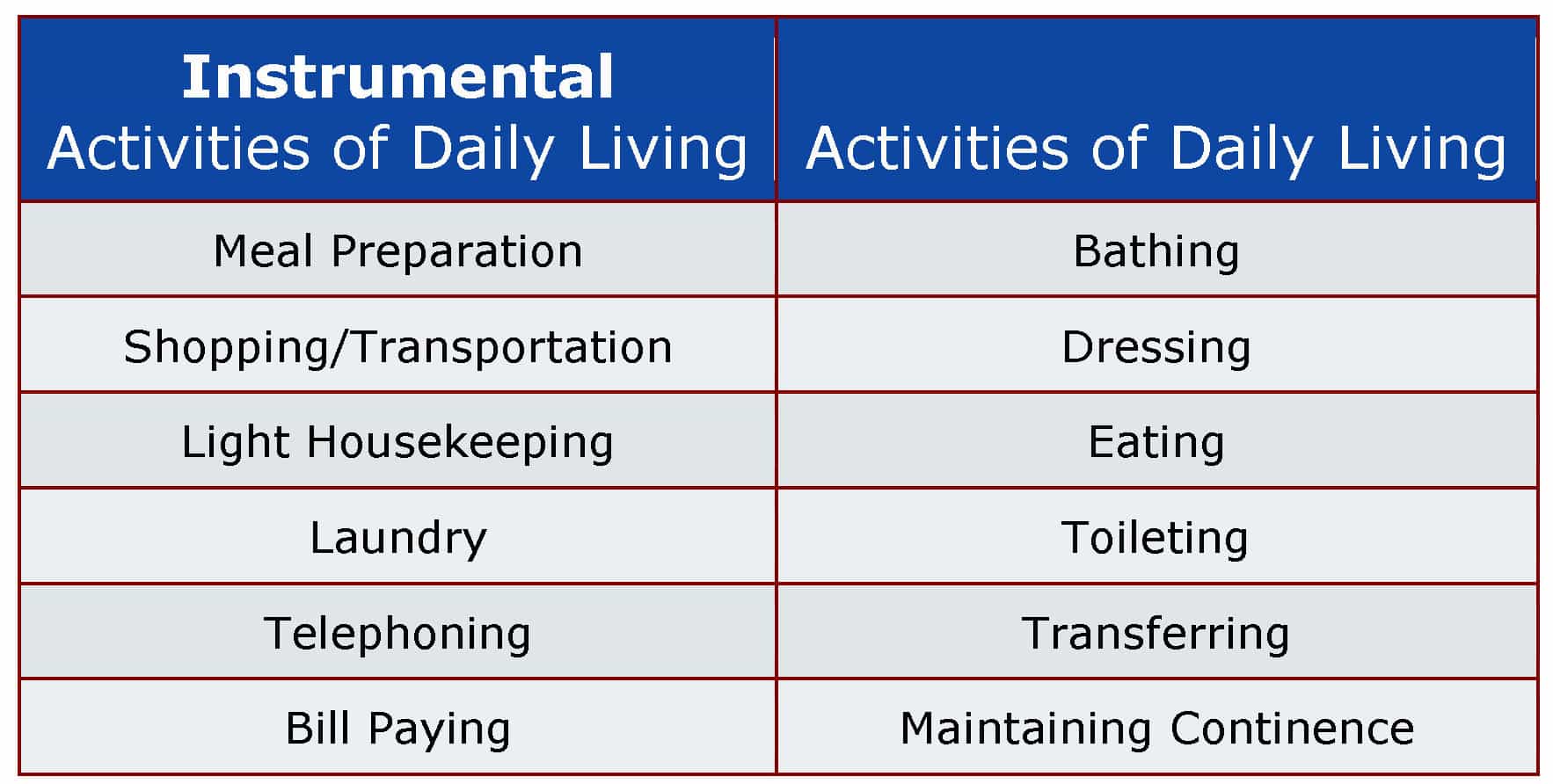

The federal government recommended, and the rest of the long term care insurance industry used, “Activities of Daily Living” to determine when a policy would pay benefits. Penn Treaty used “Instrumental Activities of Daily Living“.

Penn Treaty ignored industry standards.

Penn Treaty sold policies that ignored federal guidelines.

![]() Here are the mistakes Penn Treaty made that were in direct conflict with the standards followed by the rest of the long term care insurance industry:

Here are the mistakes Penn Treaty made that were in direct conflict with the standards followed by the rest of the long term care insurance industry:

Those of us specializing in long term care insurance have known this was going to happen for the past 15 years! When you have a company that:

- has below average financial ratings,

- offers policies with richer benefits than the rest of the industry,

- has premiums that are much lower than the rest of the industry, and

- insures applicants the rest of the industry declines,

Common sense says, “this doesn’t add up!” That is why we did NOT recommend Penn Treaty to our clients, even though Consumer Reports ranked it as the #1 long term care insurance policy!